War, Volatility, and the Repricing of Risk

March 9th, 2026

Geopolitical tensions escalated this week following attacks affecting energy infrastructure in the Persian Gulf, injecting a new layer of uncertainty into global markets. Because of its central role in global energy supply, even the possibility of disruption can ripple quickly through financial markets.

That ripple was visible almost immediately.

Volatility surged across both equity and bond markets, emerging market assets weakened, and energy prices began adjusting to the possibility of tighter global supply. These movements may appear disconnected at first glance but they reflect a pattern that often appears when markets are forced to reassess risk.

Periods of geopolitical stress tend to move through financial markets in recognizable ways. Investors first respond by adjusting risk tolerance and pricing uncertainty before deeper financial stress emerges.

This week’s developments offer a clear example of that process unfolding in real time. Later in this edition, we examine the global energy market as a case study for how geopolitical shocks move through financial markets and influence asset prices.

But first, we begin with the signals currently appearing across markets.

Market Signals: Where the Shock Appears First

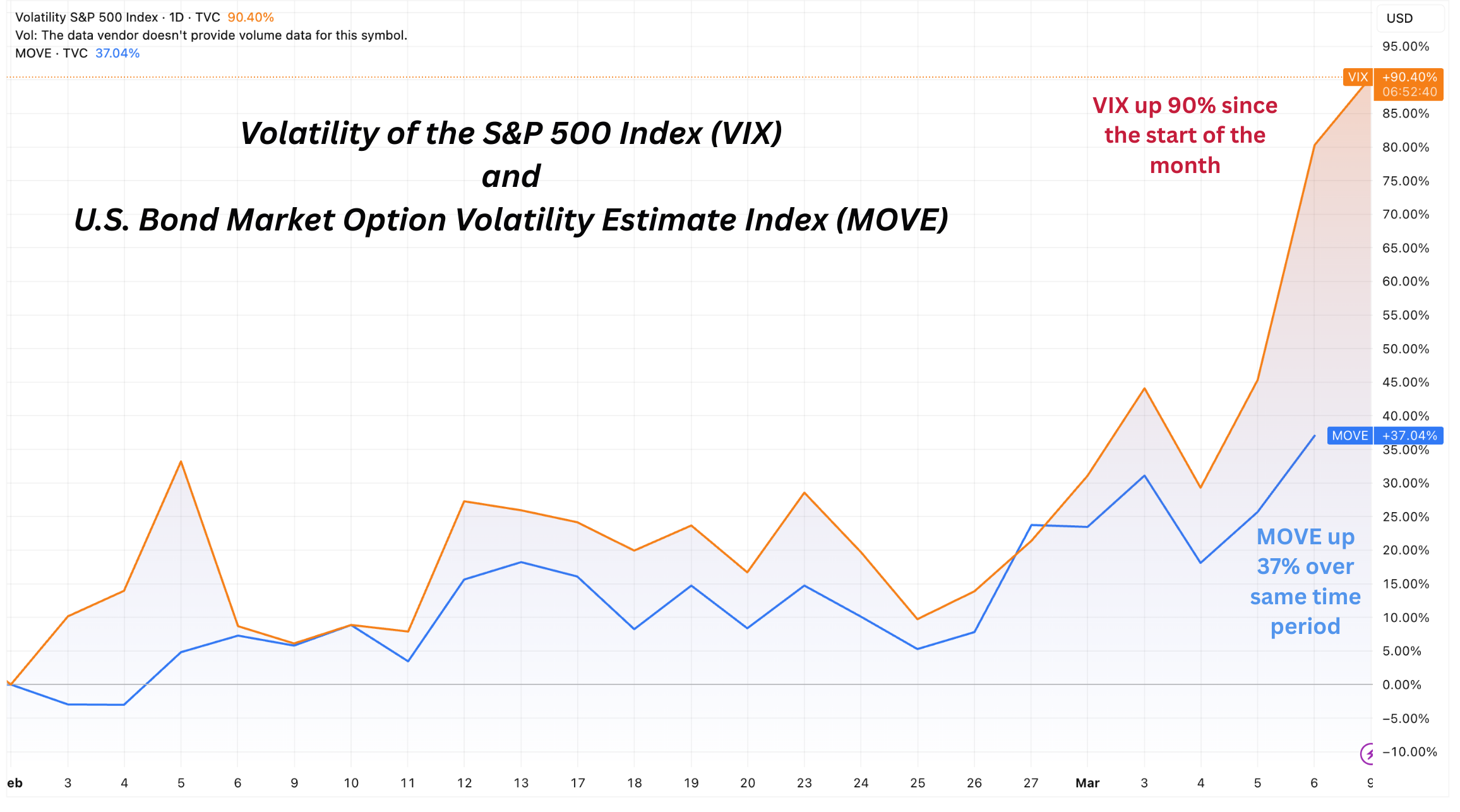

One of the earliest indicators of rising uncertainty in financial markets is a sharp increase in volatility.

That pattern was clearly visible this week.

The VIX index — which measures expected volatility in the S&P 500 — jumped from roughly 20 last week to nearly 30. At the same time, the MOVE index, a widely followed measure of volatility in the U.S. Treasury market, climbed from the low 70s to above 80.

Volatility spikes reflect a simple but important reality: when future outcomes become more difficult to predict, investors demand greater compensation for bearing risk. Markets respond by rapidly repricing uncertainty.

Beneath the surface of equity markets, additional signs of weakening risk appetite began to emerge.

The percentage of S&P 500 companies trading above their 200-day moving average declined from roughly 67% last week to about 57% this week. While the headline index moved only modestly, this deterioration in market breadth suggests that weakness is spreading across a wider share of the market.

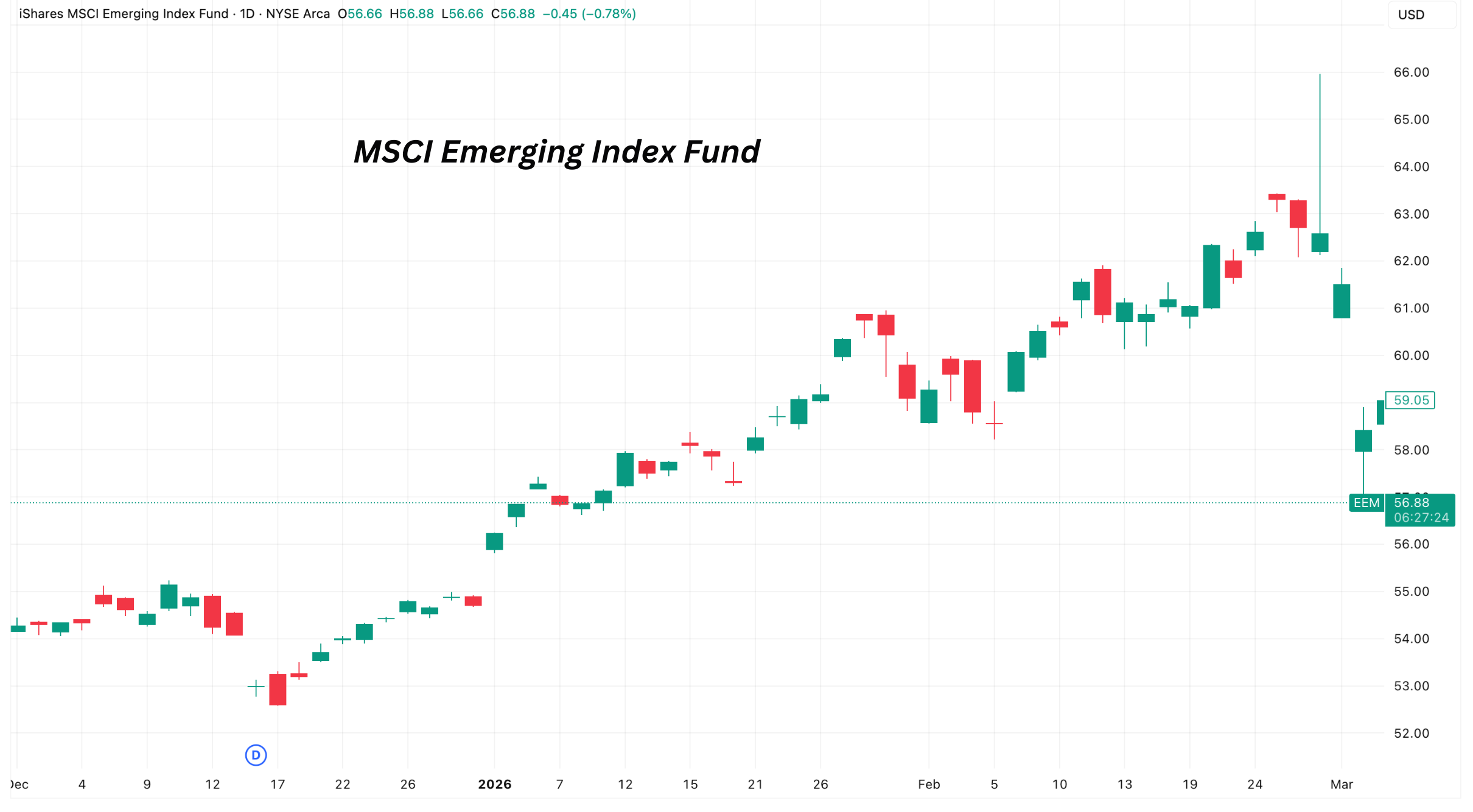

At the same time, global capital flows showed a clear shift toward perceived safety.

Emerging market equities fell sharply during the week, with the Emerging Markets ETF (EEM) declining from around $62 to roughly $57.

This type of movement is typical during periods of geopolitical uncertainty. When risks rise, capital often rotates away from regions perceived as more vulnerable and toward assets viewed as safer — particularly U.S. dollar assets and developed markets.

Taken together, these signals suggest that markets are currently responding primarily through risk repricing and volatility expansion, rather than through stress in credit or financial funding markets.

These developments are broadly consistent with the framework we discussed in last week’s edition, where stress tends to appear first in risk assets and volatility before moving deeper into credit markets or the financial system itself.

Short Case Study: The Energy Shock

Recent geopolitical developments have raised concerns about potential disruptions to energy supply in the Persian Gulf — one of the most strategically important regions in the global energy system. At the center of this concern is the Strait of Hormuz, a narrow shipping corridor through which a significant portion of the world’s oil and liquefied natural gas exports travel. Because such a large share of global energy supply passes through this route, even the possibility of disruption can quickly influence energy prices.

When tensions rise in this region, markets immediately begin reassessing the risk that supply flows could be interrupted. Energy markets are particularly sensitive to this type of uncertainty. Unlike many other industries, energy supply chains operate with limited short-term flexibility. If markets begin to anticipate tighter supply conditions — even temporarily — prices often adjust quickly.

But the market reaction is not driven solely by headlines. It reflects deeper economic mechanics embedded in global energy trade.

One important dynamic involves the structure of liquefied natural gas (LNG) markets and the role of U.S. exporters within that system. U.S. LNG producers typically purchase natural gas domestically, most commonly priced off the Henry Hub benchmark, and export liquefied natural gas to international markets where prices are frequently higher.

When geopolitical events tighten global supply expectations or increase demand for LNG shipments, international prices can move rapidly relative to domestic U.S. gas prices. In practical terms, this widens the economic spread between domestic input costs and international selling prices.

What matters in this situation is not simply the geopolitical event itself, but the economic mechanism it activates. When markets begin to anticipate tighter supply conditions, pricing dynamics shift throughout the global energy system. These changes affect producers, exporters, and energy-related equities as market participants adjust to new expectations around supply, demand, and profitability.

In this way, geopolitical shocks often act less as isolated events and more as catalysts that accelerate price adjustments already embedded in the structure of global commodity markets.

What This Episode Teaches Us About Markets

The developments of this week highlight several broader lessons about how financial markets respond to global shocks.

First, volatility tends to move before credit.

When uncertainty rises, markets typically react by repricing risk expectations. This often appears as spikes in volatility and adjustments in risk-sensitive assets before deeper financial stress develops.

Second, capital rotates toward perceived safety.

Periods of geopolitical tension frequently lead investors to reduce exposure to emerging markets and risk-sensitive assets while increasing allocations to assets viewed as more stable.

Third, real economic incentives ultimately drive market behavior.

While headlines may trigger the initial reaction, sustained market movements usually reflect underlying economic mechanisms — changes in supply expectations, shifts in pricing dynamics, or adjustments in capital flows.

Understanding these dynamics helps explain why markets often respond to global events in stages rather than through immediate system-wide dislocations.

Look out for next week’s newsletter for further insight into the forces shaping today’s markets.